J.T. Miller became the first of four arbitration-bound New York Rangers to ink a deal. On July 13th, he signed a 2-yr, $2.75m AAV contract, leaving him just one year shy of UFA status. Many have proclaimed this contract is a steal for the Rangers, but I think it is right on point. I also believe it will provide a benchmark for many of the other players lined up for arbitration right now. Thus, I have used Miller’s contract to develop a simple cap hit prediction model for those other players.

Above, in the featured image, you can see what I believe is an accurate set of data about teams with cap advantage currently on their books. All of the points represent the level of cap advantage currently accrued by the off season of any given year. For example, the Chicago Blackhawks have $31.6m in cap advantage on their books at the time of the 2016 off season. This number will be true until the first day of the season (Oct. 12), when the AAV and salary numbers stick ticking up for the 2016-17 season. I have tried graphing the correct day-to-day changes of the contracts, but it just comes out overly complicated. It’s only really important when either trades or contract terminations occur mid-season; that makes up only about 25% of events that affect cap advantage accrual to date.

If there is a problem (or praise) you’d like to share with me about this different service I am trying out, please contact me at @Chris_Beardy on Twitter, by comment below, or even on Reddit at /u/ChocolateAlmondFudge.

Yesterday I introduced Part 4 of my series on the Cap Advantage Recapture Penalty (CARP), detailing a way the League could help the Predators out of their Shea Weber cap advantage situation using available cap space in previous seasons. Today I will provide a more simple and perhaps more likely solution to the Predators’ possible future woes.

(Just a quick note, my first, second, and third posts on this topic can be found at the links provided. I highly suggest giving them a read if you need some background info on what the CARP is and how it works.)

The Collective Bargaining Agreement (CBA), which introduced the CARP has a rather straightforward passage that might be interpreted to help the Predators:

Section 50.5(d)(ii)(B)(2):Notwithstanding the provisions of Sections 50.5(d)(ii)(A) and (B), in the event that any such Long-Term Contract is Assigned during its term, each Club for which the Player plays under the terms of that Long-Term Contract shall be subject to being charged with any and all “Cap Advantage Recapture” amounts it receives pursuant to that Long-Term Contract, provided, however, that if a Club Traded a Long-Term Contract prior to the execution of this Agreement (including any binding Memorandum of Understanding) under which it gained a “cap advantage,” the “Cap Advantage Recapture” shall not apply to that Club for that Long-Term Contract. For purposes of clarity, the Club to whom such Long-Term Contract was Assigned after the execution of this Agreement (including any binding Memorandum of Understanding) shall be subject to the Cap Advantage Recapture (if any).

[emphasis in the original text]

To put it more simply: Contracts that could incur a CARP that were acquired by trade prior to the signing of the 2013 CBA will not accrue cap advantage against the recipient team.

One thing I’ve grown to appreciate is the ability of teams to find loopholes in the current Collective Bargaining Agreement. It’s fun to see how teams find a way to give themselves an upper hand over other teams (at least, until the other teams follow suit). Just now, while perusing the CBA, I came across a piece of text that could have easily been a loophole had the NHL not been more careful:

Section 50.5(h)(ii): A Club shall be permitted to have an Averaged Club Salary in excess of the Upper Limit resulting from Performance Bonuses […] provided that under no circumstances may a Club’s Averaged Club Salary so exceed the Upper Limit by an amount greater than the result of seven-and-one-half (7.5) percent multiplied by the Upper Limit (the “Performance Bonus Cushion”).

The key here is that the Performance Bonus Cushion is an allowed exceedance over the Upper Limit (more popularly known as the cap ceiling or salary cap). It does not actually change the Upper Limit. This is also the case for the Bona Fide Long-Term Injury/Illness Reserve, typically referred to as the LTIR. It is described in detail in Section 50.10(d) of the CBA:

Section 50.10(d): […] the [LTIR] replacement Player Salary and Bonuses of such additional Player(s) may increase the Club’s Averaged Club Salary to an amount up to and exceeding the Upper Limit, solely as, and to the extent and for the duration, set forth below […]

Just like the Performance Bonus Cushion, the LTIR allows teams to exceed the Upper Limit, but does not actually change the Upper Limit for that team. So why is this a big deal?

A picture of Bobby Orr probably plotting something.The metal statue in the back is likely a prototype of his cybernetics before he attempts the full conversion.

Well, let’s make up a scenario where a team can expect to have a significant amount of performance bonuses to pay out for a specific year. Let’s say that in the near future, bionic technology is mastered and Wayne Gretzky and Bobby Orr are both implanted with cyborg technology, allowing them to play at a level beyond their peaks during their dominant careers. They’re both 35+ and thus can qualify for performance bonuses of up to a maximum of $2.85m each. At $5.7m total in bonuses, you’re already at 7.8% of the 2016-17 Upper Limit of $73.0m. So what could you do? Well, if the LTIR actually changed your team’s Upper Limit then you could maneuver a player or two onto the LTIR to create $3.0m worth of cap relief. This would up your Upper Limit to $76.0m and increase your maximum allowed Performance Bonus Cushion up to exactly $5.7m.

More realistically, we see a team that has an Aaron Ekblad type of player on an Entry Level Contract (ELC) as well as a Jaromir Jagr level talent on a 35+ Standard Player Contract (SPC). And in addition, you have other lesser players on ELCs and 35+ SPCs that reach only a fraction of their potential Performance Bonuses. For example, Michal Roszival got $200k for reaching his games played threshold in 2015-16 with the Blackhawks while Teravainen made $850k for reaching various bonus milestones that same year. Panarin earned the maximum of $2.85m for the bonuses he earned. So the need for additional Performance Bonus Cushion wouldn’t be too far-fetched in my opinion.

Fortunately, this loophole is addressed with the nature of the CBA. These two mechanisms seem to have been carefully constructed to avoid this sort of shenanigans. (In addition, the Performance Bonus Cushion overage ends up rolling over to the next year’s salary cap so my hypothetical situation would have repercussions.) However, there are many incredibly smart individuals out there now working on ways to break the system for their own benefit and it will be very exciting to see how they do it.

I originally started researching and writing about the Cap Advantage Recapture Penalty (CARP) in relation to Shea Weber trade rumors last summer. It was pretty shortly thereafter that I started bandying about the phrase “Shea Weber is untradeable.” The liability of the potential CARP looming over a small market franchise like Nashville would be too great, especially considering the significant likelihood that Weber will decide not to play until he’s 41. But it happened and now I’m wrong about that. (Well, not about the CARP stuff so read on…)

(Just a quick note, my first, second, and third posts on this topic can be found at the links provided. I highly suggest giving them a read if you need some background info on what the CARP is and how it works.)

However, the exciting thing is that now everyone is talking about the CARP and want to learn more about it. I still cling to my viewpoint that the NHL has done no wrong in creating this cap mechanism. The Predators (a) chose to match the offer sheet, (b) were a party to the creation of the current CBA including the creation of the CARP, (c) chose not to buy him out with their compliance buyouts, and (d) chose to trade him with $24.5m of cap advantage sitting on their books. They made multiple conscious decisions to not limit their liability to this penalty. But, I can’t ignore the fact that others are right about how the NHL will not let a small market team, especially one that is such a major success story in their push to hockey-fy the South, be crippled with a penalty that could easily set the franchise back 5-7 years. Thirty other owner groups / GMs might say “tough nuggets” to them, but Bettman will certainly do what it takes to maintain 31 strong teams and markets in the league.

The collective bargaining agreement (CBA) agreed to by the NHL and NHL Players’ Association (NHLPA) in 2013 describes how a player can be placed on the LTIR, how this status effects his team’s cap situation, and what can be done with the player after receiving this status. In this post, I will describe how the LTIR status is granted, how it interacts with the salary cap, and provide an example of it being used in the league.

How does a player get placed on the LTIR?

The LTIR is specifically defined in Article 50.10(d) in the 2013 CBA. A player is eligible to be placed on the LTIR if the player has been determined to be unfit to play by the team’s physician for a minimum of 24 days and 10 regular season games. In the league believes that a player is being placed on the LTIR in bad faith, the league can issue a challenge. In this situation (which to my knowledge has not yet happened), the NHL and the NHLPA would select a neutral physician to evaluate the player and make a ruling.

The form needed to put a player on the IR.

What is described above is effectively a special version of the injured reserve (IR), which only requires an expectation that the player will be out for 7 days. Another key difference between the two is that the IR can be triggered retroactively and only creates a maximum roster size exception. The LTIR cannot be deemed retroactively and it can create exceptions to both the maximum roster size and the salary cap ceiling. Both statuses for a player can be designated using the form found as Exhibit 28 in the CBA, which is shown off to the side. A team would simply need to fill out this form and submit it to the NHL Central Registry and NHLPA.

Once the NHL Central Registry has approved the LTIR status, the team is allowed to add a replacement player or players to its roster.

How does the LTIR effect the salary cap?

The trickiest thing about the LTIR is determining how it effects the salary cap for a team. Article 50.10(d) in the CBA actually provides eight separate examples to demonstrate the “Bona-Fide Long-Term Injury/Illness Exception to the Upper Limit [of the Salary Cap].” Interestingly enough, the LTIR exception and the performance bonus cushion (another post for another day) create the only two exceptions to the salary cap ceiling during the regular season.

Perhaps the biggest misconception about the LTIR is that the player’s cap hit does not get removed from the team’s payroll. In fact, what happens is that the team is allowed to exceed the designated salary cap ceiling by as much as the cap hit of the contract for the player entering the LTIR. The value of the allowed overage is determined on the day that the player is moved to the LTIR. That player on the LTIR both continues to count towards the cap and continues to receive his salary. Article 50.10(d)(ii) specifically states

“The Player Salary and Bonuses of the Player that has been deemed unfit-to-play shall continue to be counted toward the Club’s Averaged Club Salary [….]”

The next Article, 50.10(d)(iii), states that

“The total replacement Player Salary and Bonuses for a Player or Players that have replaced an unfit-to-play Player may not in the aggregate exceed the amount of the Player Salary and Bonuses of the unfit-to-play Player who the Club is replacing[.]”

Finally, Article 50.10(d)(iv) states that

“[….] A Club may then exceed the [salary cap ceiling] due to the addition of replacement Player Salary and Bonuses of Players who have replaced an unfit-to-play Player, provided, however, that when the unfit-to-play Player is once again fit to play [including any time spent on a conditioning loan], the Club shall be required to once again reduce its Averaged Club Salary to a level at or below the [salary cap ceiling] prior to the Player being able to rejoin the Club [….]”

[emphasis in the original]

How has the LTIR been used in the league?

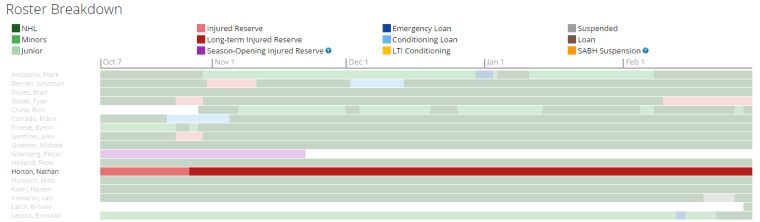

Thanks to Cap Friendly, I have found a resource that makes it a lot easier to show how the LTIR has been used this year by the Toronto Maple Leafs. They have engaged in some really interesting work with regard to cap and asset management through the use of a significant number of tools, including the LTIR. Below you can see a timeline of Nathan Horton’s status with the team over the course of the season. Most notably, he was moved from the Injured Reserve to the Long-Term Injured Reserve on October 27, 2015.

Now there had been little question from before the season that Nathan Horton was not planning to make any return to the ice. Unfortunately, he likely has career-ending medical issues, but he likely will not be retiring. It is neither in his interest (since he will continue to be paid on the LTIR) or in the interest of the Maple Leafs (for the reasons to come below) for Horton to retire at this time.

Thus the question should be asked why the Maple Leafs did not place Nathan Horton on the LTIR at the start of the season. That can illustrated with the graph below:

The black line represents the salary cap ceiling for the Maple Leafs. The blue line is their daily cap hit and the green line is a projected cap hit for the team at the end of the year. A team’s final salary cap number at the end of the year is actually the average of all their daily cap hits. The projected cap hit is that running average assuming that the current day’s cap hit were to be maintained through the end of the season.

Under normal cases, neither the blue nor the green lines are permitted to go over the black line at any single point during the season. So a team cannot operate at 150% of the salary cap ceiling for half the year and 50% of it the rest of the year to even out at 100%. No, teams must remain below the salary cap ceiling at all times. Unless they have one of two exceptions: an LTIR exception or a performance bonus cushion exception.

As mentioned above, the Maple Leafs can receive a salary cap ceiling exception equal to the overage created by the Horton contract after putting replacement players on their roster (whose total contract values cannot be greater than that of Horton’s contract), which occurs immediately after Horton is placed on the LTIR. At the start of the season, the Maple Leafs were operating at a projected $70.48m cap hit. If they had placed Horton on the LTIR at that point and fully replaced him, they could have created a maximum allowed overage of $4.38m. Instead, the Maple Leafs waited. Then on October 27, 2015, they called up Casey Bailey from the AHL (at a time when they had three players on the regular IR and needed a call-up), which put an additional $0.91m against the cap. This put the Leafs’ projected cap hit only $93,306 beneath the salary cap season. So they placed Horton on the LTIR at that point, granting them an allowed overage of up to $5,206,694 for as long as Horton is on the LTIR. (Note: Horton’s contract lasts through the 2019-20 season.) Thus, the Maple Leafs effectively have a salary cap ceiling of $76.6m while almost every other team can only spend up to $71.4m this year. (Note: Casey Bailey was back in the AHL after only two days up with the Maple Leafs. He arguably was only called up for this LTIR move.)

And so it can be seen that the Maple Leafs have used this allowed overage four separate times this year:

On October 29, 2015, they returned Casey Bailey to the minors, called Byron Froese up to the NHL, and signed Richard Clune. Overall, those moves put the Leafs at $71.5m, just slightly over the normal salary cap ceiling. This only lasted for a single day.

From December 30, 2015, to January 10, 2016, the Maple Leafs were at $71.7m in salary after an emergency call up of Mark Arcobello and Antoine Bibeau. (Both were sent back to the minors on January 3, 2015, for some reason but promptly returned to the NHL on the next day.)

From February 8, 2016, to February 22, 2016, the Maple Leafs were well above the normal $71.4m salary cap ceiling. One of the main factors was the trade that sent Phaneuf out of town (along with four other players in the AHL) in exchange for four Senators players. The exchange ultimately added $1.8m to the Maple Leafs’s salary cap. Around that same time frame, Tyler Bozak, Joffrey Lupul, and Jared Cowen (from the aforementioned trade) were all placed on the IR and required roster replacements. The Leafs ultimately carried a maximum salary cap of $75.9m on February 13, 2016. This used up $4.5m of the LTIR exception. Had Horton been placed on the LTIR at the start of the season, these roster moves could not have been done this way.

Not pictured above (because I made the image before all roster transactions were completed) is the Maple Leafs ending February 29, 2016, with about $440k above the normal cap ceiling. This is mainly related to them calling up a large number of their minor league prospects including Kasperi Kapenen and William Nylander.

Finally, it should be mentioned that sometimes the contract of a player on the LTIR can itself become a good asset. We saw that happen this past summer when Marc Savard was involved in a trade that sent him from the Boston Bruins to the Florida Panthers. The thing is: Savard has not played a single game since 2010-11, when he received a career ending concussion. So he had spent his entire time in Boston after his injury on the LTIR, which makes cap management a bit more complicated for the reasons described in detail above. However, Florida found his contract attractive as a cash-strapped team because it added $4.0m to their cap while only costing them $575k in real money each year. This helped Florida reach the salary cap floor. It was a move beneficial for both sides because now Boston has that $4.0m unlocked without having to do tricky movement of their assets.

So what next?

Well if you made it this far, you’re clearly interested in how the intricacies of the CBA. Consider taking a look at my three-part series covering the cap advantage recapture penalty. It’s just as good of a read and it covers an equally important but obscure mechanism described in the 2013 CBA.

There’s something funny about Roberto Luongo. I’m not talking about his twitter or him reading poetry about Byfuglien, I’m talking about the potential cap advantage recapture penalty (CARP) attached to his contract:

Here are the cap penalties from Roberto Luongo’s contract for the Canucks if he retires early. Could be really ugly

Yes, if Roberto Luongo retires as a Panther in 2021 (at the ripe old age of 42), then the Panthers are not hit with any CARP while the Canucks will have a one-year penalty of $8.5m. Now the explanation will be quite complex, but it’s manageable:

The Original Contract and the Trade

Below is a table of the original Luongo contract from the Canucks signed in 2010 along with calculations of AAV, annual cap advantage, and net cap advantage:

To my knowledge, there are only two teams that currently have a CARP on their books. They are the New Jersey Devils and Los Angeles Kings. The Devils have had a $250,000 penalty since 2013-14 and will have it to the end of the 2024-25 season as a result of Ilya Kovalchuk’s “retirement.” The Kings are losing $1.32m in space starting this season and running through 2019-20 due to the early termination of Mike Richards’s contract. Many teams were able to rid themselves of potential CARP-inducing contracts through the use of compliance buyouts. Compliance buyouts were two penalty-free buyouts given to each team after the 2013 CBA was signed. A tracker of these buyouts can be found here.

Let’s look at the Kovalchuk contract in more detail. Below is a table summarizing the terms of his massive deal as well as the calculation of the cap advantage associated with his deal:

Over the next few days I will be writing some articles that cover the cap advantage recapture penalty. It is something that I think is under-considered by the media and fans alike while discussing teams’ cap situations and the potential for player movement.

This introductory article will explain what the penalty is and how it is applied. Follow-up articles will give real examples of the penalty in action as well as my beliefs on how this penalty affects the league moving forward.

What is the Cap Advantage Recapture Penalty?

In addition to placing some regulations on how salary structure can be done, the 2013 collective bargaining agreement (CBA – available here) introduced a penalty to punish teams that made cap-circumventing contracts under the previous CBA signed in 2006. This penalty is called the Cap Advantage Recapture Penalty (CARP) and it basically makes sure that a team is affected by the full value of a contract should a player happen to retire early.

The reason why the CARP is a necessity is because there is a discrepancy between how players are paid and how their “cap hit” affects the team’s payroll. Starting in 2006, the CBA established a hard cap ceiling and floor for every team in the league, meaning that each teams’ player payroll had a maximum and minimum limit. Instead of using the year-to-year salaries for players, instead the averaged annual value (AAV) of each contract is used. As a result, there are seasons where the team pays players more than they are “charged” by the league. These situations are referred to as “cap advantaged” seasons. A hypothetical contract can be seen below:

{kind=link}